Once employees are caught in the financial stress cycle, they find it increasingly difficult to escape. Then, they become more stressed and their performance continues to suffer. Helping your employees escape the cycle benefits both your people and the organisation.

Recap: the financial stress cycle

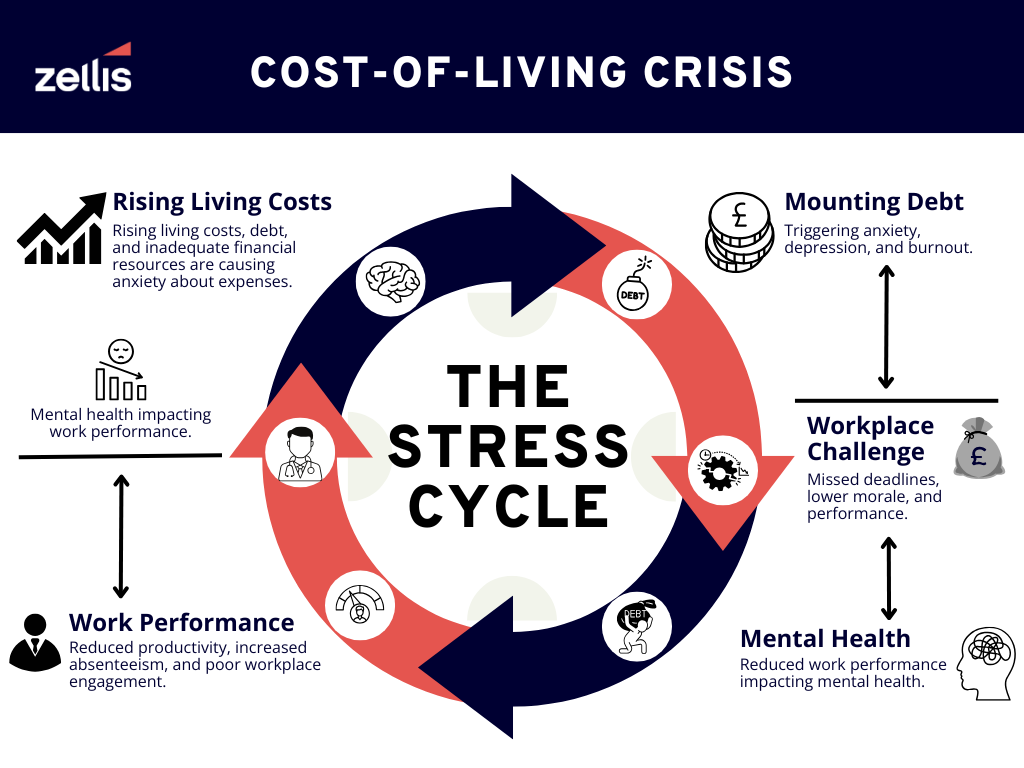

The cost-of-living crisis and associated uncertainty continues to pull more of your colleagues into the financial stress cycle. This sees a harmful spiral of rising living costs, mounting debt driving low engagement, poor mental health, and reduced work performance. A significant 77% of employees with money worries admit it affects their performance at work.

3 steps to breaking the financial stress cycle

So, what are some practical steps HR can take to disrupt the cycle and improve financial wellbeing for your employees?

1. Assess your employee financial wellbeing needs

The fact that three quarters of your colleagues are experiencing financial stress may not be obvious. You may have noticed some performance, quality and productivity issues, but the root cause is often much harder to identify.

One option is to conduct anonymous financial wellbeing surveys. A well-designed survey will also identify the specific financial stressors at work. Are your people struggling with rising costs, debts, financial insecurity?

The goal of these surveys is to show you the problems people face. The data you collect can be used to design targeted interventions, tailored to the specific needs and circumstances of the individual.

Take the example of Prudential who discovered that 34% of employees reported feeling financial stress – more than the national average. By implementing a financial wellness programme that included personalised coaching, webinars and subsidised financial benefits like childcare, they were able to halve reported stress levels across their workforce.

2. Offer comprehensive financial wellbeing employee benefits

With more people than ever caught in the financial stress cycle, HR must carefully consider the benefits packages on offer to employees. Indeed, services and tools designed to improve financial wellbeing should be a standard aspect of benefits packages. This is particularly true as 94% of employees believe that employers should provide financial wellbeing support.

But what should be included in a benefits package designed to boost financial wellbeing?

Financial education and resources

At the top of the list should be tools and training that provide employees with transparency and control over their own finances. More than simply providing a month-end payslip, employees need visibility of income and outgoings so they have a proper understanding of their financial position. These insights can then be complemented by tools that enable budget planning and financial management, like those found in MyView PayNow.

Promoting authoritative, independent information resources is also a good way to help employees improve their financial skills and answer some of their own questions (particularly those that may be too embarrassing to ask an employer). Government-backed initiatives like the Money & Pensions Service (MAPS) provide excellent advice and guidance at no charge. Simply signposting employees to these resources will help some of them on the road to financial wellbeing.

Offering value-add tools like MoneyHealth allows employees to personalise advice and guidance based on their own financial situation. With concrete guidance, your colleagues can make smarter choices and take control of their personal finances.

Supportive pay structures

Clarity and visibility are vital. Clear digital payslips should allow employees to easily view, compare, and query their pay.

This can be reinforced with flexible pay options — also known as earned wage access. Using a tool like MyView PayNow to grant employees access to some of their wage entitlements in advance can help them to cover unexpected costs. Even if your colleagues never use the function, simply knowing it is available helps to provide peace of mind – and reduce stress.

Financial resilience support

Planning for the future is just as important as solving immediate financial challenges. Providing colleagues with financial wellbeing tools that help them plan for the future will help reduce financial stress in the future too.

Introducing payroll savings schemes as part of an integrated payroll service are a great way to help employees build a rainy day fund. Or to put money towards a specific goal. Between 55% and 72% of workers say they would like to be offered a payroll savings scheme that allows them to save as they earn.

Finally, consider instituting hardship funds and employee assistance programmes. Knowing that their employer has planned for potential problems and is ready to provide help if required, provides some relief when experiencing financial stress. These schemes may also provide or signpost financial counselling to help workers regain control of their situation.

Immediacy is a critical factor in reducing financial stress. As PricewaterhouseCoopers notes in their annual Employee Financial Wellness Survey, ‘People only become more resilient once their day-to-day personal finances are under control’.

3. Measure your success

At this point, HR has a long list of potential actions to help reduce employee financial stress. But how do you know if your program is working?

Key metrics will include attendance and illness, both of which indicate potential stress in the workforce. You should also detect an increase in productivity and engagement. Freer to focus on work, your employees will achieve much more each day.

Is there an ROI associated with financial stress reduction efforts? Absolutely – along with many different ways to measure it. There will be a reduction in absenteeism, an increase in productivity and revenue per employee, and boosted employee retention. Plus, your employees will be contributing more into their payroll savings scheme.

Conclusion: Commit to financial wellbeing to break the cycle

HR leads the charge in breaking the financial stress cycle by providing the tools, strategies and impetus to empower employees. Cultural change will be a significant factor and again, HR will be pivotal in communicating the importance of financial wellbeing – and providing the necessary tools and resources to help employees regain control.

Assessing, monitoring and improving employee financial wellbeing is an ongoing process. Change will be incremental, taking time to achieve significant results. However, the sooner your business begins the process, the better – implementing just one change will yield results and set the stage for further improvement.

Investing in financial wellbeing to break the financial stress cycle creates a positive ripple effect throughout the organisation. Both employees and organisations benefit when stress is brought under control.

Key takeaways

- Financial stress is widespread and impacts employee performance.

- Assessing wellbeing needs should be a key priority.

- A comprehensive financial wellbeing package will help to bring stress under control.

- Innovation and technology will help to keep financial wellbeing programs manageable.

- Measuring KPIs will be central to assessing gains for you and your colleagues – and for helping direct future improvements.

Ready to break the stress cycle?

Learn more about how to fight the effects of financial worries and how to change the situation in From stress to success. How to enhance workplace financial wellbeing.