On 1st October, Minister for Finance Jack Chambers TD and Minister for Public Expenditure and Reform Paschal Donohue TD delivered Budget 2025 at Dáil Éireann. We dive into the detail with Seán Murray, Director of Product Services, setting out what it means for payroll in Ireland.

Budget 2025 Ireland: an overview

The measures outlined in this year’s Budget amount to a 7% increase in spending when compared to last year. Disposable income was once again a focus, with increases to tax credits, standard rate cut-off points, and the 2% threshold for the universal social charge (USC). There was also a reduction of the USC 4% rate to 3%, which will all see employees receive an increase in net pay come the first pay date in January.

A rise in the national minimum wage (NMW) of 80c per hour will benefit the lower paid. Coupled with the increase in the 2% USC earnings threshold, it should ensure that anyone on the NMW and a maximum 39-hour working week will remain on the lower rate of USC.

Some employers will be impacted by the uplift in NMW, which will increase labour costs slightly. Employers in hospitality were hoping that the Minister might consider a reduction of the 13.5% VAT rate to the 9% pandemic-era level. Unsurprisingly, this change didn’t materialise. However, employers will be relieved to hear that Minister for Social Protection Heather Humphreys has announced a further delay in the rollout of the proposed pensions auto-enrolment scheme to 30th September 2025.

Budget day also brought in a previously announced 0.1% increase to PRSI contribution rates for both employees and employers. This was the first in a series of annual increases, which will accumulate to a total increase of 0.7% by 2028. The purpose of this initiative is to replenish the Social Insurance Fund in preparation for an expected increase in demand for the state pension as more people reach the accessibility age.

Seán Murray, Director of Product Services at Zellis, gave this overview:

“A not too dissimilar Budget to last year. It will be broadly welcomed by employees and employers alike. This is a pre-election Budget after all. Employees will benefit from an increase in net pay in 2025 due to the tweaking of tax and USC thresholds, and pensioners will receive a €12 per week increase as a result of the social welfare package. Meanwhile, employers will be receptive towards some of the growth initiatives, such as the increased threshold in the R&D tax credit, the two-year extension of the Employment Investment Incentive, and the Start-Up Relief for Entrepreneurs. Undoubtedly, hospitality will be disappointed that their lobbying for a reduction in the VAT rate hasn’t borne fruit, but it’s understood that some form of discussion is ongoing behind the scenes.”

Now for a closer look at the key changes in Budget 2025…

1. Tax credits and cut-offs

While income tax rates remain the same, as expected, the Minister has announced some tweaks to standard rate cut-off points and tax credits. These changes aim to put more money into the pockets of PAYE workers:

The standard rate cut-off points were increased by €2,000.

The standard rate cut-off point for the calculation of tax for employees on the emergency basis was increased by €38 per week or €166 per month.

Personal, employee, and earned income tax credits all increased by €125 each.

What does this mean for payroll?

Employees will realise the benefits from the rises in the standard rate cut-off points and tax credits from 1st January, when they receive their 2025 tax certificates. We expect these certificates, or Revenue Payroll Notifications (RPNs), to be available from the Revenue Commissioners in week two of December. Employers may download the certificates at this point and apply them to payroll for processing in tax period one of 2025.

For Zellis customers: the statutory parameter table for tax will be updated as part of the ROI legislation upgrade in November, to reflect the above changes.

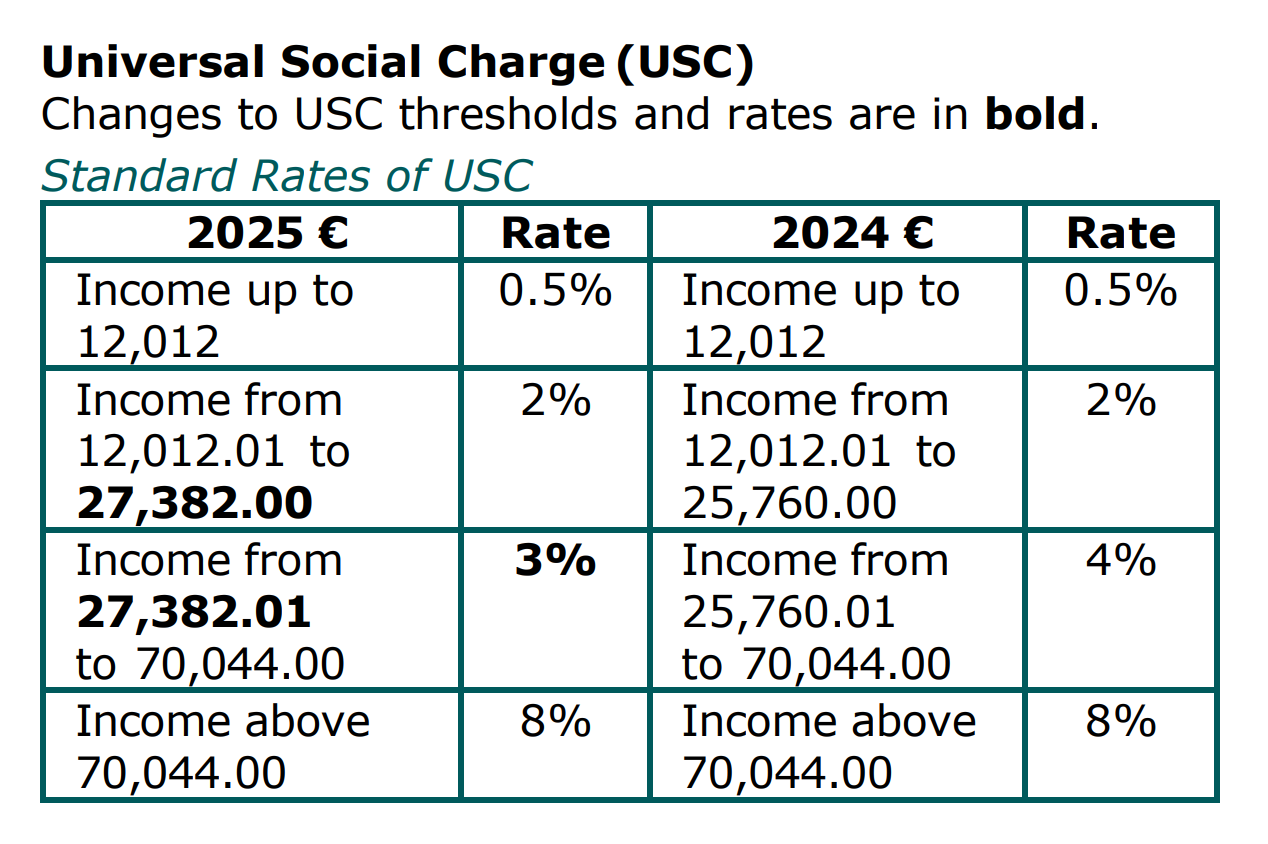

2. Universal Social Charge (USC)

The Minister delivered further relief for employees via amendments to the USC rates and thresholds:

The middle rate of USC fell from 4% to 3%.

The entry point for this rate will increase by €1,622, in line with the increase to NMW, so it will apply to income between €27,382 and €70,044.

The above change will ensure that employees who are in receipt of the new national minimum wage for a 39-hour week remain on the lower rate scale for USC.

The USC exemption earnings threshold of €13,000 remains unchanged.

The emergency USC rate of 8% also remains unchanged.

What does this mean for payroll?

Similar to the tax changes, employees will feel the benefits from the amendments to the USC from 1st January, when they receive their 2025 tax certificates. These RPNs should be available from Revenue in week two of December. Employers may download the certificates at this point and apply them to payroll for processing in tax period one of 2025.

For Zellis customers: we will update the statutory parameter table for USC as part of the ROI legislation upgrade in November, to reflect the above changes.

3. PRSI (effective 1st October 2024)

In last year’s Budget, the government made an unprecedented move by giving one year’s notice of PRSI rate increases effective from 1st October 2024. This change, featured in our recent blog on PRSI changes in Ireland, is now live, increasing of 0.1% to employee and employer rates.

The plan is for these PRSI rate increases to continue annually until 2028. However the postponement of pensions auto-enrolment might have an impact. One year’s worth of lost contributions could mean that the current schedule of PRSI increases falls short of raising enough for the Social Insurance Fund, to maintain the pension retirement age at 66.

What does this mean for payroll?

PRSI rates increased with effect from 1st October for pay dates falling on or after this date.

For Zellis customers: the statutory parameter tables for PRSI were updated automatically back in September in anticipation of this change. At the same time, we issued our on-premise clients with instructions on how to implement these changes themselves.

4. Company car benefit-in-kind

The government is very much continuing with its drive to incentivise businesses to ‘green up’ their fleets. The lower the CO2 emissions rate of a vehicle, the lower the rates of benefit-in-kind (BIK) tax. The Minister maintained the following measures:

The temporary universal relief of €10,000 to the original market value (OMV) of a vehicle was extended by a further year to 31st December 2025.

The existing €35,000 OMV reduction for electric vehicles (EVs) was extended for 2025.

The 4,000-kilometre reduction in the highest mileage band was extended until 31st December 2025.

Taken together with the extension of the universal OMV relief of €10,000, an employee with a company EV will continue to see an overall benefit-in-kind OMV relief of €45,000 in 2025.

The government also introduced a BIK exemption for expenses incurred by an employer in providing EV charging facilities at the home of a director or employee.

What does this mean for payroll?

In effect, there are no changes for employers who are already incorporating the above OMV reduction provisions into BIK calculations for company cars.

For Zellis customers: The ROI BIK Administration module already caters for the above OMV provisions. No change required to the BIK statutory parameter tables. (ROI BIK Administration module is available to customers who have licensed it).

5. Small Benefit Exemption

A much welcome change will be the increase to the Small Benefit Exemption limit from €1,000 to €1,500 per annum per employee. The number of benefits an employer may give has also increased from the current limit of two to five. These benefits must be non-cash and must not exceed an aggregate value of €1,500 in a tax year.

What does this mean for payroll?

Employers may wish to review their current policies concerning small benefits and consider any monitoring to track cumulative small benefit values.

6. National Minimum Wage

The NMW will increase by 80c from €12.70 to €13.50 per hour. This change comes into effect for hours worked on or after 1st January 2025.

What does this mean for payroll?

Employers should ensure they check that any reports tracking payments against NMW are compliant with the new hourly rate.

7. Statutory Sick Leave

In line with the Sick Leave Bill 2022, statutory sick leave entitlement increases from five to seven days, effective from 1st January 2025. The Department of Social Protection is yet to confirm this change.

What does this mean for payroll?

Employers operating statutory sick leave should check that the correct annual entitlement is assigned to each employee from 1st January 2025.

8. Additional Superannuation Contributions (ASC): public sector employers only

The Department of Public Expenditure and Reform (DPER) has confirmed there are no changes to rates and thresholds in 2025.

What does this mean for payroll?

There is no impact.

For Zellis public sector customers: no action required. The values for ASC in the statutory parameter tables for 2024 will carry forward to 2025.

9. Pension auto-enrolment

There will be a further delay to the rollout of the pension auto-enrolment scheme, to 30th September 2025.

What does this mean for payroll?

Employers, HR, and payroll personnel should familiarise themselves with the provisions within the Automatic Enrolment Retirement Savings System Bill. Organisations should check the impact on any existing company pension scheme offered to staff, scheme rules, and entry criteria to that scheme. Employers should also check the likelihood of employees joining the state scheme, based on the eligibility criteria for auto-enrolment. Consider also the likely cost impact of the state scheme and mandatory employer contribution rates.

Note and further information

The above is our interpretation of the forthcoming changes as announced in the Minister’s Budget 2025 speech. It is not intended to constitute tax, financial, or legal advice. The measures are subject to change ahead of the passing of the Finance Act.