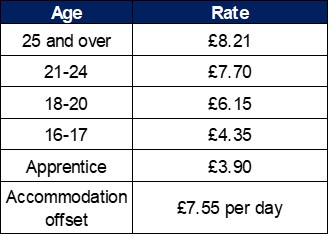

National minimum/ living wage

Despite what all the guidance from HMRC says, the new rates of national minimum/living wage didn’t necessarily come into force on 1 April. The legislation says that the new rates are effective for the first period beginning on, or after, 1 April. So, if you pay your weekly paid employees for a week that runs from Sunday 31 March to Saturday 6 April, you don’t need to bring the new rates into effect until the pay week beginning Sunday 7 April. The new rates are as follows:

The voluntary living wage, which is not mandatory, rises to £9 per hour outside London and £10.55 in London from April 2019.

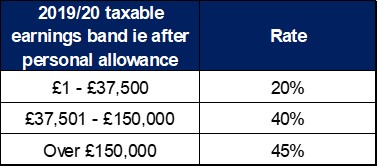

Tax rates, bands (and countries!)

The Chancellor increased the personal allowance to £12,500, a year early in his budget last October, and unusually it will be the same for the following tax year (2020/21) as well. this means the monthly tax threshold to 2019/20 is £1042. There is no change to the £100,000 income limit where the personal allowance starts to be withdrawn on a 2:1 ratio, so for 2019/20 the personal allowance will be fully removed when someone has total income of £125,000 or more. He also increased the 20% tax band, for England, Wales and Northern Ireland so that 1/2m fewer people will pay 40% tax in 2019/20. The new bands are:

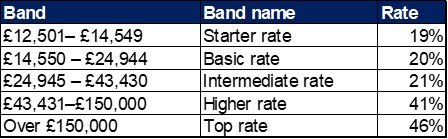

Scotland has devolved powers to set its own rates and bands of income tax and these have now been agreed as follows for 2019/20:

For the first time in 800 years Wales has income tax raising powers from the start of the 2019/20 tax year. Westminster removes 10% from each of the bands and the Welsh Assembly sets its own rate per band. They have decided to set the Welsh rate of income tax at 10% for 2019/20. So, whilst Welsh taxpayers will see no difference in the tax that they pay, as compared to taxpayers in England and Northern Ireland, 10% of the tax raised in each band will go directly to the Welsh Assembly to invest in public services in Wales. This will only happen though if HMRC have identified the Welsh taxpayer and issued them with a tax code prefixed with a C.

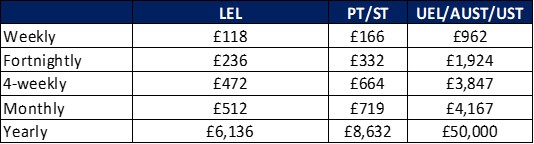

National insurance

The rates and table letters for national insurance are unchanged for 2019/20, but the thresholds have been uplifted by inflation as follows. The increase in the UEL to £50,000 means that some employees will save 20% on their tax as the drop out of the 20% tax band, but pay 12% NI rather than 2%.

Student loans

Postgraduate loans for English and Welsh student begin to be deducted through the payroll from April 2019. An employee earns £25,725 or over they will pay 15% student loan deductions if they have both a Plan 2 undergraduate loan and a postgraduate loan. The Plan 2 threshold increases to £25,725, with deductions at 9% on all Ni’able pay over the threshold, and the postgraduate threshold is £21,000 ,with deductions at 6% over the threshold. To facilitate the introduction of postgraduate loans the starter checklist has been updated and can be found here. Make sure you’ve stopped using the 2016 version from 6 April 2019.

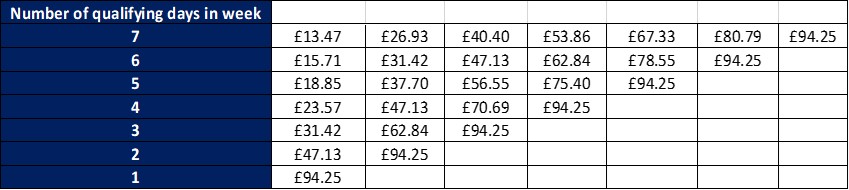

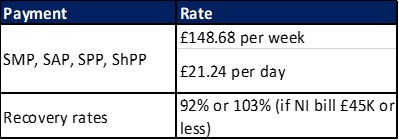

Family and absence related statutory payments

The new rates of statutory sick pay come into effect on Saturday, 6 April, whilst the family related rates increase from Sunday, 7 April as statutory payment weeks for maternity, adoption, paternity and shared parental pay always begin on a Sunday. The new rates are

Apprenticeship levy

This remains at 0.5% with the levy allowance set at £15,000 which can be split across connected companies/charities.

Payroll is complex, and getting it right is crucial. Does your payroll software keep you compliant with the latest legislation? Visit Zellis at the CIPD Festival of Work on 12-13 June 2019 for a demo of how our solutions can keep your payroll running correctly on time, every time: Book your demo here