The role of the CFO is changing. As with nearly every area of life and business, the significant shifts brought about by the COVID-19 pandemic have had a major impact on many finance leaders’ day-to-day priorities and activities.

This means that their focus is no longer simply on cost control and the financial health of the organisation. Today there is just as much emphasis on how to manage and mitigate risk and build resilience within the business at all levels.

What’s pressuring CFOs, and how are they responding?

Key to building this resilience, according to our research report entitled ‘The Resilience Factor: CFOs. Post-COVID Boardroom Insights 2021’, which was based on a survey of 125 CFOs in the UK and Ireland, is having a finance leader who is willing, ready and able to embrace change.

A major consideration in this context is that ‘change-ready CFOs’ tend to be more risk-aware than their less adaptable peers. During the various lockdowns, two out of five of such finance leaders reported the need to personally focus on tackling regulatory compliance issues – an unfortunate burden when their attention was needed elsewhere.

The most significant of these challenges in terms of risk to the business was reviewing supplier relationships (49%). It also became clear that organisations that had implemented supply chain risk management processes prior to the pandemic were in considerably better shape to handle the ensuing crisis than those that had not.

From keeper of the coffers to a catalyst for change

Next on the risk management challenge list, meanwhile, was ensuring operational efficiency (43%) and managing business continuity (BC) risk (42%).

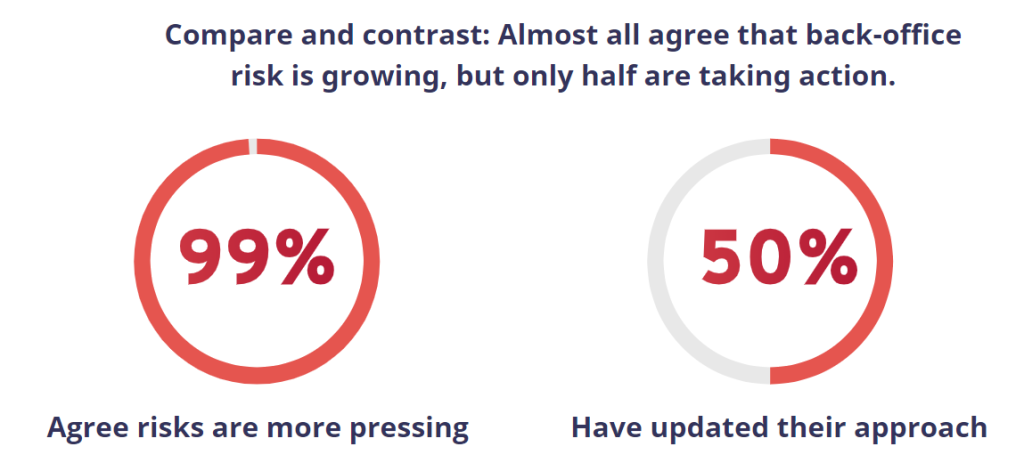

In terms of the latter, a huge 99% of CFOs acknowledged that BC risk relating to back-office activities, such as payroll, had become an increasingly pressing matter over recent years. Despite this situation, as few as 50% acknowledged having ‘fully’ updated their approach in this area. A further 26% admitted to having done so only ‘partially’, which means it is still a work in progress across the UK and Ireland.

As for the year ahead, CFO key priorities appear to be changing slightly. The number one item on the list is tackling operational efficiency (44%), followed by enabling regulatory compliance (38%), managing BC risk and reviewing supplier relationships (at 37% respectively).

Upgrading technology (36%) was ranked among the top five as growing numbers of finance leaders recognise the risk mitigation opportunities offered by everything from cloud-based systems to managed services.

There is also a growing understanding that digital transformation when combined with the reworking of old and outmoded business processes has the potential to unlock greater levels of efficiency, boost agility and enable finance leaders to employ data more effectively.

Using data in this way not only helps to inform business strategy and identify any resilience issues before they become a problem. It also opens up the possibility of exploring new business areas and creating new revenue streams.

Which means that the role of CFO is not only changing to adopt a role insulating the business from unpredictable risk but is increasingly becoming a catalyst for change too.

For more statistics and analysis, including our top three recommendations to CFOs who recognise people, processes, and technology as key priorities for investment, download the full report here.