This 2023 research has been updated with a 2025 survey. Find the results of the new research here.

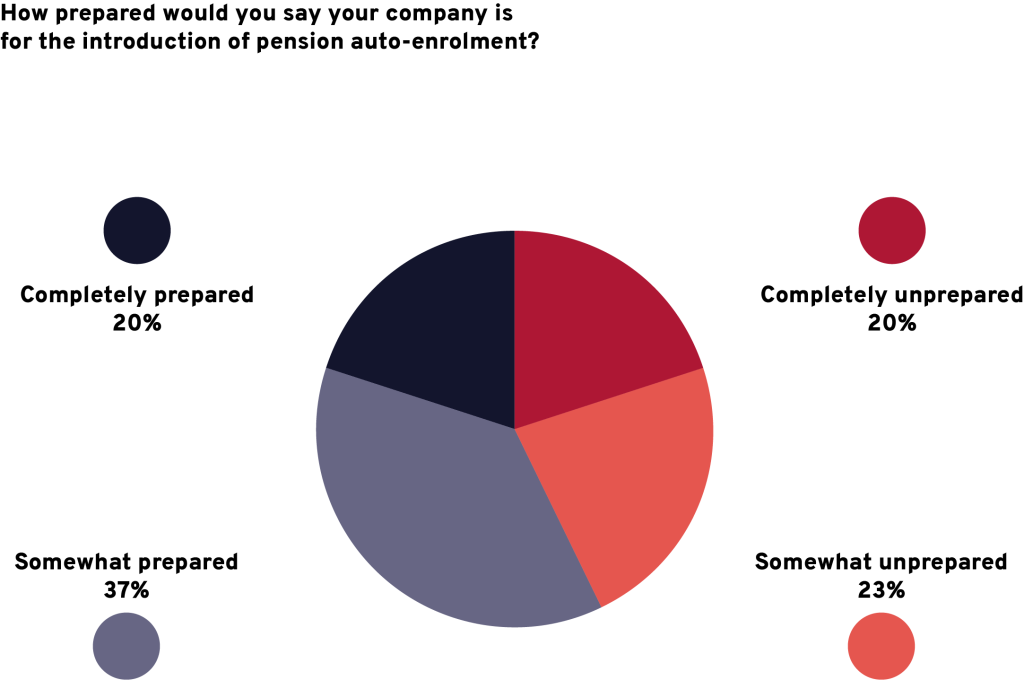

Although the rollout of pension auto-enrolment in Ireland is quickly getting closer, only one in five payroll and HR professionals feel totally ready for the impending change.

By way of contrast, some 43% say they are either ‘somewhat’ or ‘completely’ unprepared for it, according to new research by Zellis Ireland. To make matters worse, a huge 50% indicate they have ‘very little’ or ‘no’ understanding of what the scheme will actually mean in practice.

The full findings are all in our new report ‘Prepared for pension auto-enrolment? How employers in Ireland should get ready for rollout.’ The results come from a 2023 survey of 500 payroll and HR professionals in Ireland, across a range of sectors.

The study explored readiness for the government’s Automatic Enrolment Retirement Savings System, set to cover 750,000 private sector workers. To be eligible, they will need to earn more than €20,000 per annum and not be part of another occupational pension scheme. The first contributions must be paid in January 2024. Amounts will increase gradually over the course of 10 years.

Find a detailed explainer of the new scheme here: Ireland pensions auto-enrolment: Guide for payroll and HR

Widespread unpreparedness for pension auto-enrolment in Ireland

Despite looming deadlines, a mere 28% of the employers questioned have so far worked out the cost implications and how to finance them – although 44% are part of the way there.

A further 28% have done no such forecasting at all, although the financial implications are expected to be significant in most cases. These include employer contributions and the administration and labour costs involved in implementation.

Only 31% of organisations have made sure their payroll system can make the necessary calculations, deductions, and contributions. These go to the Central Processing Authority (CPA): responsible for overseeing and operating the scheme.

Moreover, only 27% respectively have updated their employment contracts or created a communications plan to inform employees of the pension system, fund options and any tax implications.

Learnings from the UK auto-enrolment scheme

Irish employers can benefit from the experiences of their UK counterparts, who have already gone down the auto-enrolment route. Pension uptake was high and is currently running close to 80% compared with only 47% in 2012. By 2021 employer contributions for more than half of all eligible staff in most industries were above the statutory requirement.

At a more practical level, after working with thousands of employers on the UK rollout, Zellis’ internal experts have gained a number of useful insights. Their three key suggestions for ensuring your implementation is successful are:

1. Don’t underestimate the time and effort required

Challenge: Many UK employers underestimated the work involved and delayed their preparations. But enrolling the entire workforce into a scheme and then administering it can require significant time, effort, and investment.

Recommendation: Bring together a team of key stakeholders as soon as possible and devise a plan of action.

2. Communicate and engage with the workforce

Challenge: Failure to communicate early, clearly and frequently with employees made the transition more difficult for UK employers and created problems further down the line.

Recommendation: Ensure HR and internal communications teams work together – with payroll and finance where appropriate – to create an ongoing employee information plan.

3. Watch out for compliance pitfalls; the devil is in the detail

Challenge: While the big picture requirements for this kind of legislation are often clear, problems tend to emerge when dealing with the detail. For example, UK employers were required to offer staff a voluntary opt-out. But giving it too much prominence or presenting it as the ‘easier option’ was not allowed and risked penalisation.

Recommendation: Dedicate enough time and headcount to fully understand all requirements, and be prepared to communicate with the relevant authorities and experts if clarification is required.

Collaboration is key to getting ready

Close collaboration between payroll, HR, and finance is imperative to make such a complex initiative successful. Each plays an important role. Payroll should be responsible for providing and processing accurate pay data. Also for deducting the correct contribution amounts for both employees and employers.

HR is accountable for updating employment contracts to reflect the new pension arrangements and informing staff of the new scheme. This includes it will affect their pay and what their options are. The role of finance is to take control of forecasting and budgeting.

We can help you prepare for pension auto-enrolment in Ireland

Another crucial part of the mix is your payroll provider. Not only should they upgrade their software system to ensure compliance. But they should also be able to offer you advice and support with the transition process, particularly if they have prior auto-enrolment experience.

Zellis not only provides market-leading Irish payroll software, but also offers managed payroll services, which can vastly reduce the administrative burden for organisations.

Find out more in the full auto-enrolment reports:

2025: The final countdown. How to get ready for pension auto-enrolment in Ireland

2023: Prepared for pension auto-enrolment? How employers in Ireland should get ready for rollout