In early October, Minister for Finance Michael McGrath TD and Minister for Public Expenditure and Reform Paschal Donohue TD delivered Budget 2024 at Dáil Éireann. The package amounts to a cost of €14 billion. The clear theme is easing the pressures of the cost-of-living crisis.

Increases to the standard rate cut-off points and tax credits, as well as favourable adjustments to the universal social charge (USC) rates and thresholds, will see a welcome boost in disposable income for most.

A rise in the minimum wage and USC threshold adjustment to ensure that those on lower incomes remain exempt from the higher rates will also be welcome.

From an employer point of view, there were no amendments that would give cause for concern regarding increasing labour costs, although we anticipate employer rate increases later in the year.

With a general election to nominate a 34th Dáil on the horizon, it’s no surprise that Budget 2024 contained something for everyone. Although not a giveaway bonanza for voters feeling the pressure of inflation and price rises on their disposable incomes, it did contain a number of reliefs for taxpayers in the form of increased tax credits and rate band cut-off points as well as a reduction in USC.”

Seán Murray, Director of Product Services, Zellis Ireland

Employees will get an increase in net pay on their payslips, and pensioners will benefit from a €12 weekly increase. Plus, there are energy credits for all in the form of three €150 instalments.

7 key changes for Irish payroll in Budget 2024

1. Income tax

The total income tax package introduced is worth €1.3 billion. Contrary to certain rumours, Minister McGrath did not announce the introduction of a third rate of tax. The standard rate of 20% and higher rate of 40% will continue to apply. What’s changed is:

- The standard rate cut-off points were increased by €2,000

- The standard rate cut-off point for calculation of tax for employees on the emergency basis was increased by €38 per week or €166 per month

- Personal, employee and earned income tax credits all increased by €100 each.

What does this mean for payroll?

Employees will realise the benefits from the rises in the standard rate cut-off points and tax credits from 1st January, when they receive their 2024 tax certificates. These certificates, or Revenue Payroll Notifications (RPNs), are likely to be available from the Revenue Commissioners in week two of December. Employers may download the certificates at this point and apply them to payroll for processing in tax period one of 2024.

Note that for Zellis clients, the statutory parameter table for tax will be updated as part of the upgrade to R31A in November to reflect the above changes.

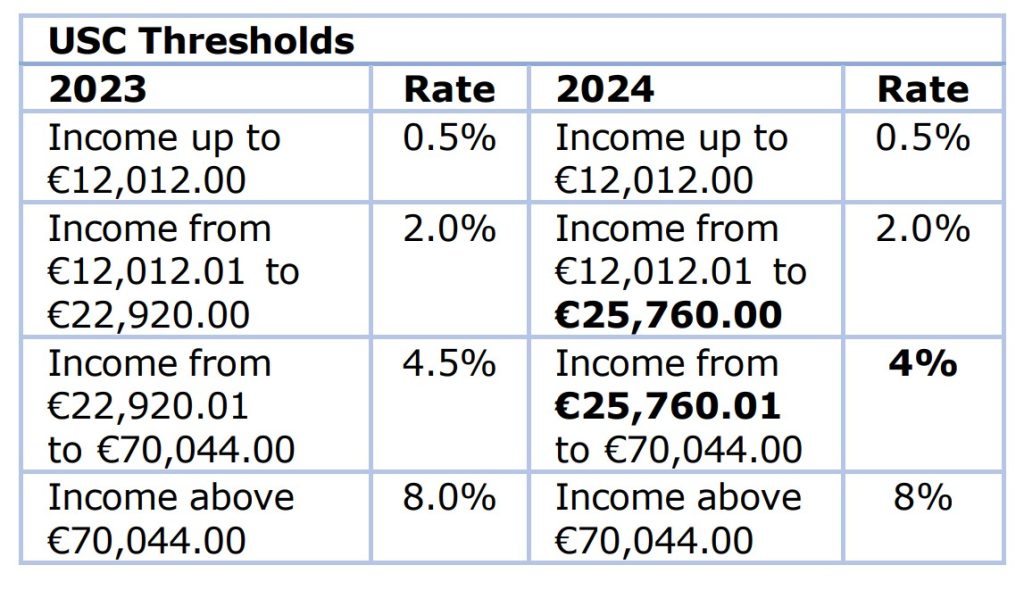

2. Universal Social Charge (USC)

The Minister delivered further relief for employees via amendments to USC rates and thresholds as follows:

- The middle rate of USC fell from 4.5% to 4%

- The threshold for entry to the 2% rate of USC rose to €25,760, thus ensuring that employees who receive the new national minimum wage for a 39-hour week remain on the lower rate scale for USC

- The USC exemption earnings threshold of €13,000 remained unchanged

- The emergency USC rate of 8% stayed unchanged

What does this mean for payroll?

Similar to the tax changes, employees will feel the benefits from the amendments to the USC from 1st January, when they receive their 2024 tax certificates. These revenue payroll notifications (RPNs) are likely to be available from Revenue in week two of December. Employers may download the certificates at this point and apply them to payroll for processing in tax period one of 2024.

Note for Zellis customers: We will update the statutory parameter table for tax as part of the upgrade to R31A in November to reflect the above changes.

3. PRSI (rise effective 1st October, 2024)

In a slightly unprecedented move, the Minister has given advance notice of an increase in pay-related social insurance (PRSI). This will come into effect from 1st October, 2024. It’s likely that this will come in the form of a 0.1% rise in both the employee and employer rates.

This measure looks like the first step to address what Minister McGrath referred to as the “long-term sustainability challenges faced by the state pension system.” Further increases are probable over the coming years.

Minister for Social Protection Heather Humphreys TD reinforced the point by adding, “In order to meet the additional costs of retaining the pension age at 66, it is important that we begin to address the long-term sustainability challenges faced by our pension system with phased increases to PRSI rates.”

The comments from both ministers suggest that this may be the ‘thin edge of the wedge’ and a forewarning of what is to come in the shape of further PRSI increases in future budgets, to help stock the war chest required to service increasing state-pension costs. With the planned introduction of pension auto-enrolment next year, the government will be hoping that the measures will serve as a two-pronged attack on a looming state-pension funding crisis.”

Seán Murray, Director of Product Services, Zellis Ireland

What does this mean for payroll?

An upgrade to PRSI rates will be necessary ahead of the 1st October, 2024 effective date. As a rise in employer rates is also on the cards, employers should consider the cost implications and plan for these.

4. Company car benefit-in-kind tax

The government is very much continuing with its drive to incentivise businesses to ‘green-up’ their car fleets. The lower the CO2 emissions rate of a vehicle, the lower the rates of benefit-in-kind (BIK) tax. The Minister introduced the following measures:

- The temporary universal relief of €10,000 to original market value (OMV) of a vehicle was extended by a further year

- The existing €35,000 OMV reduction for electric vehicles was extended for 2024 and 2025

- The 4,000-kilometre reduction in the highest mileage band was extended until 31st December, 2024

Consider also the extension of the universal open market value (OMV) relief of €10,000. Together, this means an employee with an electric company vehicle sees an overall BIK OMV relief of €45,000 in 2024.

What does this mean for payroll?

For employers already incorporating the above OMV reduction provisions into their calculations of BIK for employees availing of company cars, then no changes are required.

Note for Zellis customers: For those currently using the ROI BIK Administration module, the software already caters for the above OMV provisions.

5. Share-based remuneration consultation

The Minister also announced that the Department of Finance plans to launch a public consultation on share-based remuneration. This recognises the importance companies place on share schemes as a way of retaining and rewarding employees. It also goes along with an increasingly globalised workforce.

What does this mean for payroll?

There are no immediate changes in the coming year for how share-based remuneration is to be treated for taxation purposes.

For any employers who pay shared-based remuneration, the Minister has expressed a strong interest in hearing from all stakeholders when the public consultation process commences.

6. National Minimum Wage

The Minister introduced a rise in the minimum wage from €11.30 per hour to €12.70 per hour.

What does this mean for payroll?

Employers should ensure any reports currently processed that track payments against minimum wage comply with the new hourly rate.

7. Statutory sick pay (SSP)

In line with the Sick Leave Act 2022, the Minister brought extended the entitlement from three to five days, with effect from 1st January, 2024.

What does this mean for payroll?

For employers operating statutory sick leave, checks now should ensure the correct annual entitlement is assigned to each employee from 1st January, 2024.

For a closer look at SSP, including further changes for 2025 and 2026, see our guide for payroll and HR.

While Budget 2024 brings several relief measures, the question remains as to whether they have gone far enough to relieve the pressure on the ‘squeezed middle’, who are bearing the brunt of ongoing mortgage interest rate increases, rising house prices, and general inflation. In the face of these challenges, will further emergency measures be required in the form of an interim budget before this government completes its term? Only time will tell.”

Seán Murray, Director of Product Services, Zellis Ireland

Note and further sources

The above is our interpretation of the forthcoming changes as announced in the Minister’s Budget 2024 speech. It is not intended to constitute tax, financial, or legal advice. The measures are subject to change ahead of the passing of the relevant legislation, the Finance Act.

Full details of the measures can be found in Budget 2024 Summary (Revenue) and Irish Government Guide to Budget 2024.

Discover more legislation and compliance guidance

Work Life Balance Act 2023: Guide for Irish payroll and HR

Irish Revenue Enhanced Reporting Requirements (ERR) guide

The final countdown: Ready for pension auto-enrolment in Ireland?