For company cars that are registered from 6 April 2020, employers will be using new CO2 emission values as a result of the move to the worldwide harmonised light vehicle test procedure (WLTP). This is a new CO2 emissions testing regime developed after the VW scandal to replace the New European Driving Cycle (NEDC), which was last updated in 1997. It is part of the government’s move to introduce new rules in respect of ultra-low emission vehicles (ULEVs).

In the Autumn Budget 2017, the Chancellor announced changes to the taxation of ultra-low emission vehicles which are provided as company cars. These changes were included in the Finance Act 2017 to take effect for tax year 2020/21 and for subsequent tax years. Section 139 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA) provides the basis of the formula for calculating the percentage related to the CO2 emissions for cars emitting less than 75g/km of CO2.

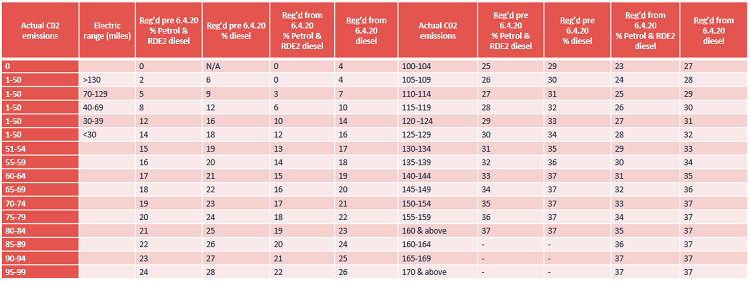

From 6 April 2020 there will be different CO2 emissions based on the ‘electric range’ of hybrid cars. The electric range means the maximum distance in miles that the car can be driven in electric mode on one battery charge. The five new bands for hybrid cars emitting up to 50 g/km of CO2 are based on kilometre equivalents that are specified in either:

- An EC certificate of conformity

- An EC type-approval certificate, or

- A UK approval certificate

It is one of these three documents which allows a car to be registered.

Fully electric cars will have a zero car benefit charge for 2020/2021.

Also included in the Autumn Budget 2017 was a decision to move to the WLTP. As this was not ratified immediately the legislation is included in Finance Act 2019, which is currently making its way through Parliament. The changes will take effect for tax year 2020/21 and subsequent tax years. The CO2 emissions for cars that have over 50 g/km of CO2 emissions will differ for cars registered before 6 April 2020 and from 6 April 2020. In the consultation about the move to WLTP, the government estimated that 50% of company car users would see an increase in their company car tax benefit of between 10% and 20%.

To mitigate this for the next two tax years, percentages will be reduced as cars will move into a different emissions bracket than under the old regime, as accessories such as air conditioning and sunroofs will move the car into a higher emissions bracket as it makes the car less fuel-efficient. Cars registered before 6 April 2020 will continue to hold their CO2 figure under the old NEDC regime for the life of the car.

P11D changes

Next autumn, ready for the 2020/2021 P11D submission, HMRC will make changes to section 5A of P11D working sheet 2 and section 3A of working sheet 2B.

As well as indicating the zero emissions mileage for hybrid cars in meeting 1–50 g/km, the fuel type when the car is not in electric mode will dictate the appropriate percentage. Fuel types A (petrol) and F (RED2 diesel so-called ‘clean diesel’) will attract a percentage that is four percentage points lower than cars using old-style diesel. A car that is RDE2 compliant will be shown as such on one of the three conformity certificates shown above.

The relevant percentages are as shown below

Payrolling cars

Employers who have made the decision to payroll their company cars will need to include the zero emissions mileage range for hybrid cars emitting between 1-50 g/kilogram CO2 emissions in the full payment submission (FPS) the date first registered from April 2020.